Is China Golden Classic Group (HKG:8281) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that China Golden Classic Group Limited (HKG:8281) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China Golden Classic Group

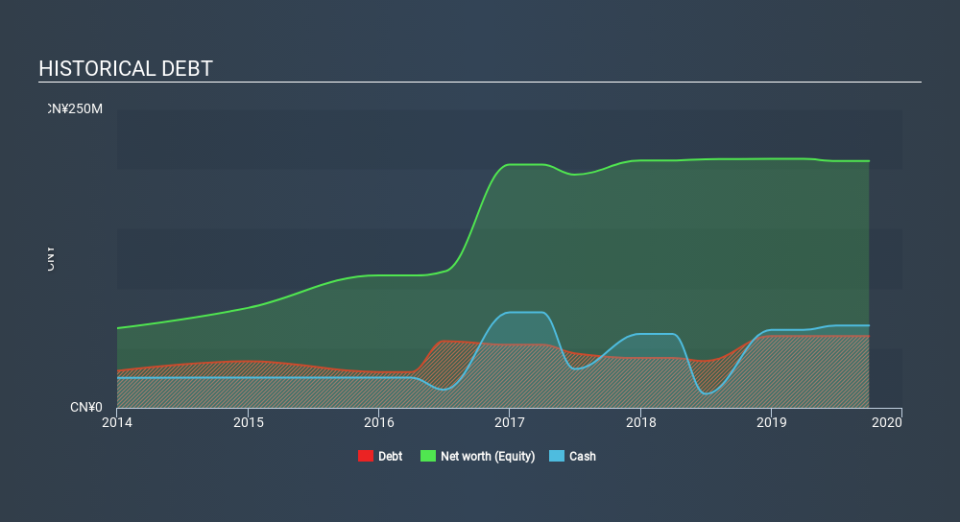

How Much Debt Does China Golden Classic Group Carry?

The image below, which you can click on for greater detail, shows that at June 2019 China Golden Classic Group had debt of CN¥60.0m, up from CN¥39.2m in one year. However, it does have CN¥68.8m in cash offsetting this, leading to net cash of CN¥8.84m.

How Strong Is China Golden Classic Group's Balance Sheet?

We can see from the most recent balance sheet that China Golden Classic Group had liabilities of CN¥142.7m falling due within a year, and liabilities of CN¥428.0k due beyond that. Offsetting these obligations, it had cash of CN¥68.8m as well as receivables valued at CN¥35.7m due within 12 months. So its liabilities total CN¥38.6m more than the combination of its cash and short-term receivables.

Given China Golden Classic Group has a market capitalization of CN¥205.4m, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, China Golden Classic Group also has more cash than debt, so we're pretty confident it can manage its debt safely.

Importantly, China Golden Classic Group's EBIT fell a jaw-dropping 57% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is China Golden Classic Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While China Golden Classic Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, China Golden Classic Group actually produced more free cash flow than EBIT over the last two years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While China Golden Classic Group does have more liabilities than liquid assets, it also has net cash of CN¥8.84m. And it impressed us with free cash flow of CN¥29m, being 119% of its EBIT. So we are not troubled with China Golden Classic Group's debt use. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 4 warning signs with China Golden Classic Group (at least 1 which doesn't sit too well with us) , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.