Should Acrow Formwork and Construction Services (ASX:ACF) Be Disappointed With Their 16% Profit?

Passive investing in index funds can generate returns that roughly match the overall market. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). To wit, the Acrow Formwork and Construction Services Limited (ASX:ACF) share price is 16% higher than it was a year ago, much better than the market decline of around 6.2% (not including dividends) in the same period. If it can keep that out-performance up over the long term, investors will do very well! Acrow Formwork and Construction Services hasn't been listed for long, so it's still not clear if it is a long term winner.

Check out our latest analysis for Acrow Formwork and Construction Services

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

During the last year, Acrow Formwork and Construction Services actually saw its earnings per share drop 46%.

So we don't think that investors are paying too much attention to EPS. Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

We think that the revenue growth of 19% could have some investors interested. Many businesses do go through a phase where they have to forgo some profits to drive business development, and sometimes its for the best.

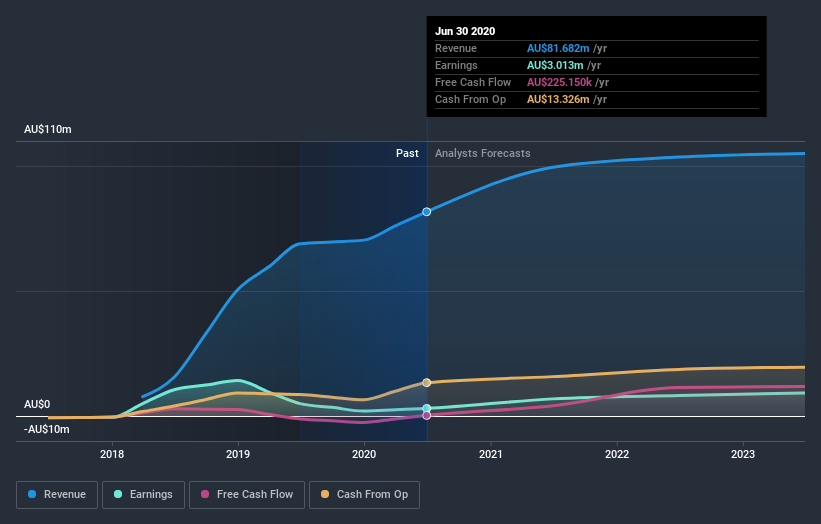

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. If you are thinking of buying or selling Acrow Formwork and Construction Services stock, you should check out this free report showing analyst profit forecasts.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, Acrow Formwork and Construction Services' TSR for the last year was 20%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

Acrow Formwork and Construction Services shareholders should be happy with the total gain of 20% over the last twelve months, including dividends. A substantial portion of that gain has come in the last three months, with the stock up 20% in that time. This suggests the company is continuing to win over new investors. It's always interesting to track share price performance over the longer term. But to understand Acrow Formwork and Construction Services better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 6 warning signs for Acrow Formwork and Construction Services you should know about.

Acrow Formwork and Construction Services is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.